Experience the world of

Advanced and Secure

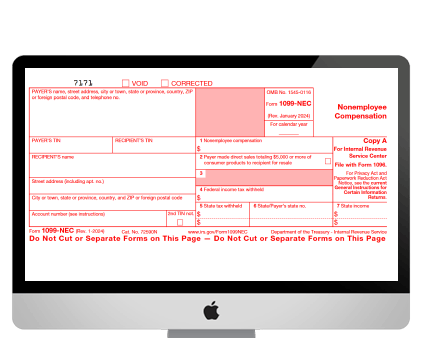

e-filing of 1099 forms

Efile saves paper and it's cost effective

Simple, quick and secure efiling of 1099 forms

Simple

Secure

E-Filing

$0.55 /form

Affordable Prices

Exclusive Features

Bulk Import

TIN Match

Premium Support

FREE Tech Support

Tax Practitioner

Bulk Upload

$0.55 /form

1099online will transmit your e-filed return to the IRS same business day.

Only 3 steps to E-File form 1099

FREE REGISTRATION

Simply click on "REGISTER" and start entering your filing information. Pay only when you click on submit to e-file. If you're a tax preparer or other third party filer, easily manage tax filing for multiple accounts in single registration.

ENTERING THE 1099 DATA

It takes less than 10 minutes to enter your payer, payee and 1099 form information via our easy to use navigation process. You can also review your 1099 form before submitting it to the IRS. Large filers can use our bulk data upload feature to save time.

ONE CLICK E-FILE TO IRS

That's it you are done. Review your information and click submit to IRS/State. Make your payment and a confirmation e-mail will be sent to your email address about your status. The IRS acceptance status will also be emailed to you once the IRS processes your filing.

As low as

$0.55cents/formWhat more we offer

Smart Features Exclusive features

Why Customers us!

Thank you very much for your wonderful support, it's incredible.

Thomas

The program is great, but what impressed me the most was the service you provided.

Marilyan